Somewhat OT but nonetheless…Unless you quote the relevant paragraph/s that indicate that SANS 10400, and/or relevant amendments, apply retrospectively to existing buildings without further extension or addition to the previously approved building and services, I believe you are mistaken in this interpretation and, for me, has the potential to cause suspicion about why this type of message comes from your industry - and possibly dilutes the positive parts.

SANS is a standard, not a law. Even without debating phrasing the implication of your interpretation would have somewhat ludicrous consequences. When needing to comply with XA2 (At least 50% (volume fraction) of the annual average hot water heating requirement shall be provided by means other than electrical resistance heating") the problem is actually the element and not the cylinder - i.e. if only your element packs up you will be required to replace/supplement your electric geyser with whatever alternative is deemed to meet XA2.

If my house/roof orientation is East/West I will likely also now be forced to install a heatpump as a solar (thermal) hot water heater is unlikely to satisfy the requirements. So, in this case “the law” requires that when my electric geyser element stops working, I have to install a heatpump?

It would also mean that if the kids break a window, I can’t replace the broken pane without first checking the glazed area to floor area, and if exceeding 15% now I also have to possibly replace more glass and even the entire frame to meet the fenestration requirements?

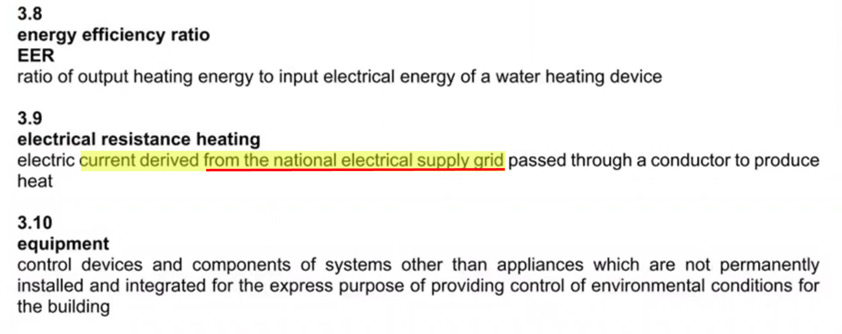

Also intersting for me is how XA2 has become a blanket “no electric element allowed” mantra. The SANS 10400 definition of “electrical resistance heating” actually appears to say something different:

As it reads now, the problem is not the method but the source of supplying the method. If 50% of the heating is done with “none-grid derived electricity” XA2 should still be complied with so, if having ample surplus PV that feeds a traditional electric geyser this should also satisfy XA2.

I do however agree that ideally in situations where means allow:

Apologies if I unnecessarily state the obvious. You will need to determine what the exact priorities are for you/family and then how your budget will allow to cater for that. You will also need to include an unbiased evaluation of for instance the area where you live - even if not liking the local council how do you judge the upkeep of the infrastructure etc.

If prolonged local outages seem to be a once in 5 years type thing, then it is probably not a priority for now to add stacks of panels and batteries. If reducing monthly electricity expenses comes out top, then look what source is most likely to achieve that. If electric water heating is the main contributor, then that will be the place to change/spend.

If having some redundant electricity supply available comes out top, then battery and PV and/or generator are likely the places to look

Also look wider than the obvious replacing eskom electricity with other electricity. If being more focussed on the potential for a prolonged electricity outage, having a gas hob might be more useful than more battery (even in bad weather you can cook and heat water…even useful if water supply is interrupted). If wanting to reduce winter monthly heating costs a proper wood burning closed combustion stove might give you more than trying to increase your PV/inverter/battery to cater for electric heaters. Maybe a very efficient dishwasher, where you rather wash dishes every 2nd/3rd day will have more impact (should cut down on both water and heating costs).

Not to go into this any further - SANS 10400 XA2 is a deemed to satisfy standard, refered to by the NBR which is the law, with certain mandatory requirements that need to be adhered to. Thats that. You are correct in almost all your examples mentioned, however it comes down to a system. Replacing a window pane - you are replacing part of a system (building envelope) with a functional replacement. That does not require you to comply to the new regulations because the system currently installed (constructed) remains the same. The same with replacing a geyser element - you are not touching the system, you are replacing a non - functional part of an existing system with a new functional part in the existing system.

Now - say you actually change the size of the window you are replacing in a house - making it bigger - then you need to apply SANS 10400 XA2 to that change, because you are making a" change " to that system, which now must be tested against SANS 10400 XA2, if its part of the building envelope off-course. The same counts for making the room bigger or adding a room. However all areas that was not touched, don’t need to change.

The same now coming back to your geyser. If you need to replace your geyser, you are replacing a system, not part of a system and that is where you are supposed to apply Deemed to Satisfy regulations, and in this scenario you should consider something more energy efficient. This is why it was mentioned as it where, and there is definitely no ill intention in the statement coming from my profession. You can do with it as you please

I think my insurance company will argue the geyser is a PART of the hot water system when they see the replacement cost and see the costs of a XA2 replacement. I won’t something 5x the replacement cost of a normal geyser.

Insurance companies will look at putting you back in the position you were before the damage occurred, and will most likely not pay out more than conventional quoted products, until it becomes a industry standard - like it is to replace a laptop with the current like - for - like model, and even TVs, where a certain model without Netflix get replaced with a smart tv because there are no others left. It will come down to yourself, and your personal needs. there is no municipal police in this country standing ready to tell you to replace this and that because you are not complying. You start thinking about it because you are forced to, due to the electrical crises we are experiencing and the cost implications of running a conventional geyser vs energy efficient alternative. Nobody is going to go out and replace their current systems because someone said its redundent. But you will consider doing so once your existing system blows up as example. Insurance will currently cover only what you had - but I will give my insurer a call tomorrow and ask about this, and if i get a proper answer I will post it here

I had an insurance claim for burst pipes in Ireland about twelve years ago.

The ceilings had to be replaced in several rooms.

The insulation standards have changed since the house was built. The insurance company replaced the insulation with the new (far thicker) insulation over the affected rooms.

But only over the affected rooms.

This was done without my intervention.

Sometimes maybe even a little better if they are feeling generous

Little off topic but my mountain bike has a carbon frame, it is insured with Discovery, after a accident that resulted in a crack on one section of the frame I put in a claim.

Discovery notified me that the carbon repair guys found 2 other cracks that where not related to the claim, but since it can compromise the integrity of the whole frame they are going to pay for the repair of those too.

On topic though:

I recently added lagging to my SWH since it had about 3m of metal pipe just exposed to the elements, it has made a dramatic improvement in the speed at which “hot” water comes out of the tap.

Insulating Exposed pipes makes a huge difference. Its part of the system that has the biggest heat loss.

also the distance to the furthest point of the building.

That’s my feeling as well. So they will want to put in another geyser (possibly a slightly better insulated one) in the place of the old one.

It is a bit like when I have a total loss scenario (written off) with a car. The insurance isn’t buying me a new one. They are giving me the value of the old one. Whatever extra I need to buy something that complies with my current and future needs, is for my own pocket. And when that means money out of my pocket at a time I cannot really afford it… that is my problem.

This is why I asked about where insurance stands on the matter. Because if insurance companies take the same approach to geysers as they do to cars, and on top of that there is now a law that requires me to buy a better car (by analogy), that’s going to hurt an awful large number of consumers. I mean, we can accept that a man who has the capacity to buy a car can be expected to buy a smaller/older one or do without, but are we expecting poorer households to do with half the hot water as before… is hot water a luxury on the same level?

I’m being philosophical, I realise that. But normally, if you want to know what the law says, you can always look at what the insurance industry is doing… if they are ignoring it, odds are it can be ignored

No, I think it’s not the same. When there’s a claim they have factored in the price of a new geyser. Remember there’s the ‘excess’ that one pays when you have a claim. This will ensure the insurance companies stay in business no matter what…

And even then, there may be an lower limit. I have “excess waiver” on my cars. I don’t pay an excess. But I still cannot claim for anything under 2k… I think.

With Discovery you can even have them give you 100% of your fuel spend in value if you let them pay it into your “excess funder” account.

I did that and after 3 months when I had a little over R3k in there covering any excess that would come from a claim I switched it back to receiving 50% of my spend in hard cash

Excesses can also be done as a form of “self-insurance”. The higher the excess, the more risk to oneself, and premiums drop substantially.

We have an “excess fund” and it earns interest for us. That is if we don’t use it and then a claim hits us.

If one does the effort and do the sums, in and around what to insure, what excesses, man, you can save a ton of money. Like I have never insurer my cellphone. Some things are cheaper to “carry the risk yourself” than pay for it over decades.

Jup.

The low-hanging fruit … claims under X amounts cost the same amount of time, effort … admin. So “get rid of them”, add an excess, or terms and conditions … focus on what insurance is actually for.

My 2 cents.

Titbit:

Insurance is not “voodoo”, nor “out to get you” … it is a very well-regulated industry that needs qualifications and has the law behind it, for it, an “ombudsman” too. I know that for a fact. Some people I know write the law books for it.

And yes, as with all and every big financial industry, there is criminal activity. WHEN it comes out, there are always serious consequences, for the insurer/broker and client.

Start rant:

The problem is … no-one reads the #($*% copious amount of documentation that insurers/brokers must send out, by law. Then they B&M after the event not having bothered to even check what they bought cover for. End rant.

Re Excess Waiver. I did the math. At the time we had a “prang” (a mild accident, a fender bender) roughly once every two years. I did a quick multiplication sum in my head, discovered that the excess waiver costs less than the excess, and went with it.

Shortly afterwards, our accident rate dropped to about 1 in 5. Because, you see, the insurance company knows far better than me what my real risk is over the longer term.